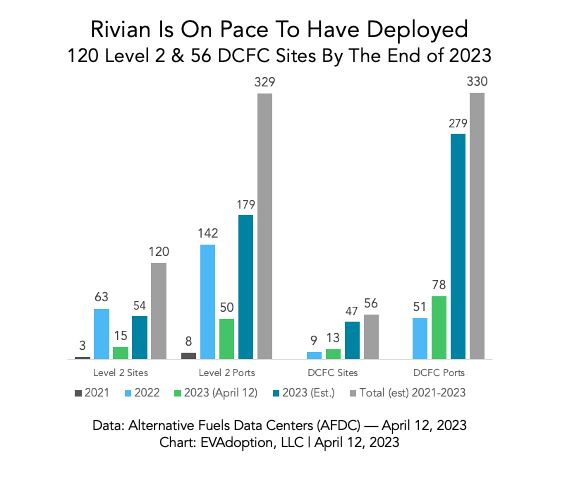

The Rivian Adventure Network (DC fast charging) could end 2023 as the 7th largest DC fast charging network in the US and is on pace for the #5 slot in 2-3 years. Rivian’s typical DCFC site has 6 DC fast chargers.

“We’re installing 3,500+ of these chargers at approximately 600 sites along popular routes.”

— Rivian

Mercedes-Benz is also launching a DC fast charging network in the US. Why are these automakers investing so much capital and resources in EV charging infrastructure? Because unlike the gas car/truck and gas station model — at least at this stage of the market you cannot separate EV charging from the EV itself. The best customer experience results when the entire charging process is designed for the driver of a specific EV brand.

This will of course change over time as we have more standardization, Plug and Charge gets adopted widely, more high-powered chargers are deployed and the EVs can accept those charge rates, and of course reliability and uptime improves.

I continue to argue that the main reason to buy a Tesla is because of its two charging networks — Supercharger (DCFC) and Destination Charging (Level 2) — and it is no coincidence that Tesla’s BEV sales share of the US market and DCFC share are both north of 60%.

I don’t expect many other (if any – though there are rumors that Hyundai may launch its own network) automakers to launch their own branded charging networks. But I do expect them to take on a greater role in the ecosystem and more strategic partnerships like GM’s Ultium Charge 360 partnership with EVgo.