EVgo released its Q2 2024 earnings on August 1 with several key highlights, including reaching a 20 percent average utilization in the quarter and expectations to reach EBITDA profitability in 2025.

Among the metrics and highlights that stood out and were of most interest to us from the 35-page Q2 2024 investor presentation, included:

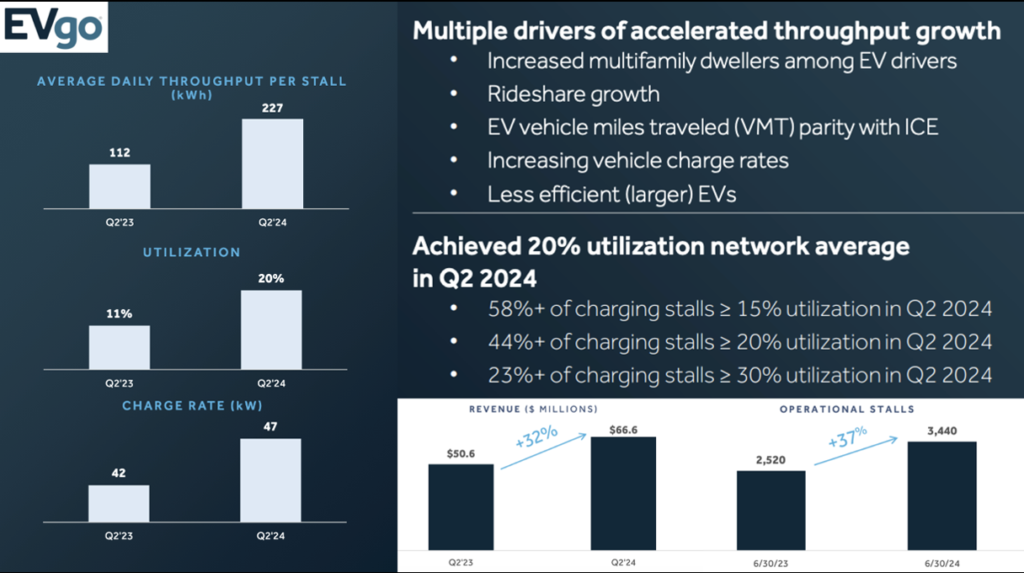

- Utilization increased to 20% from 11% in Q2 2023 and 19% in Q1 2024. And most impressively, 23% of EVgo’s fast-charging stalls had a 30% or greater utilization rate.

- The average daily kWh throughput per stall doubled to 227 kWh from 112 kWh in Q2 2023 and 193 kWh in Q1 2024.

- The average charge rate increased to 47 kW from 42 kW in Q2 2023, and 43 kW in Q1 2024.

- Rideshare, OEM charging credit, and subscription plans accounted for 56% of throughput in Q2 2024. This is the same percentage as Q1 2024, but the Q2 2024 presentation lists “Rideshare growth” as a key trend, but did not break out that percentage. In the Q1 2024 investor deck, rideshare throughput was 24% of throughput in Q1 2024. So while EVgo did not share the rideshare throughput percentage for Q2, our assumption is that rideshare driver sessions are increasing and accounted for at least 25% (one quarter) of kWh throughput in Q2 2024.

- The number of operational stalls grew 37% to 3,440 from 2,520 in Q2 2023.

EVgo did not share specific numbers, but the company also cited an increased number of sessions from multifamily dwellers, and an interesting combination of higher kW charge rates along with more larger and less-efficient EVs.

From a revenue perspective, Q2 2024 saw an increase of 32% to $66.6 million from $50.6 million in Q2 2023. And the adjusted EBITDA loss improved by $2.6 million to -$8 million from -$10.6 million. The company is solid from a cash perspective, ending Q2 2024 with over $162 million in cash, cash equivalents and restricted cash.

EVgo’s guidance for the full year 2024 is to reach $240M to $270M in revenue and adjusted EBITDA losses of $(44M) to $(34M). While EVgo is still losing money, it expects to reach breakeven in 2025 based on EV VIO (vehicles in operation) growth, continued EVgo network growth, and continued execution of operational efficiencies.

There are a lot of fascinating metrics above from EVgo’s Q2 2024 investor presentation, but a few that we found of particular interest include:

1) That one-fourth of the kWh throughput in Q2 2024 was from rideshare drivers. This trend of increased charging by rideshare drivers is good for the financial health of fast-charging networks/CPOs but can lead to wait times for non-rideshare drivers, especially at busy stations. Active rideshare drivers may often have 1-3 charging sessions per DAY, whereas a local apartment dweller may only need to charge 1-3 times per WEEK.

EVgo does not break out detailed charging session data by types of drivers, however, it appears that much of the company’s (as well as Electrify America’s, Tesla’s, and other networks/CPOs) significant increase in utilization in the last year or so substantially stems from rideshare drivers.

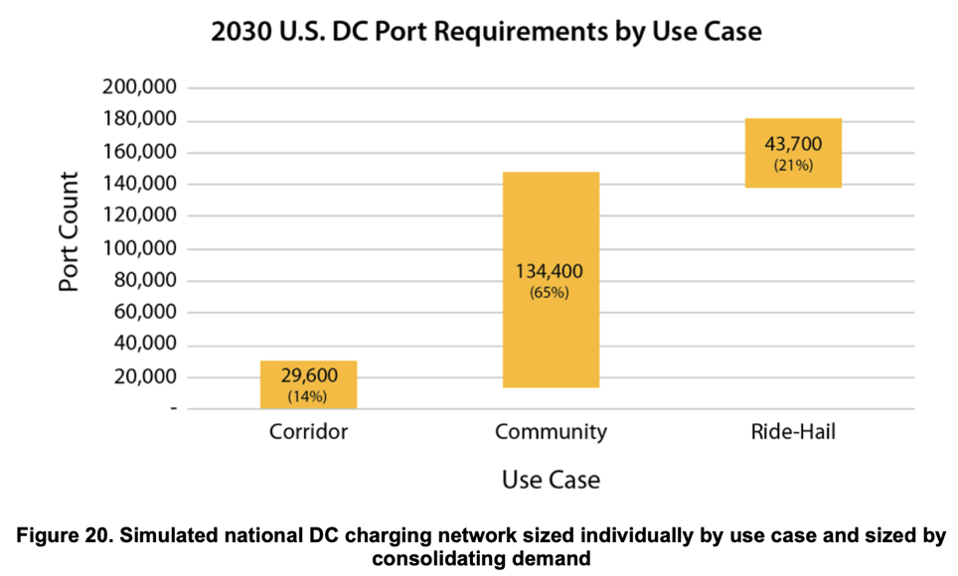

Interestingly, NREL’s 2030 forecast for DC fast chargers needed in the US included 43,700, or 21% of the total, just for ride-hail vehicles. According to NREL, if the three use cases in the chart below are modeled in isolation, the US would require about 208,000 DCFC ports. But when combining the three use cases for shared use (as is the case in the real world), the number decreases to 181,500 ports (an efficiency improvement of 13% enabled by shared use).

Using NREL’s forecast, if rideshare drivers continue using public chargers designed for general use, the US would need 26,500 fewer DCFC ports, than if the estimated 43,700 needed just for ridehail drivers, were built just for that use case.

But this forecast by NREL combined with the EVgo numbers suggests an emerging issue the industry needs to address. Ridehail drivers are using public fast chargers as part of their business, even if the drivers are not employed by Uber, Lyft, et al. These drivers are in essence part of a commercial fleet. Should these drivers be allowed to charge their EVs at the same charging station as someone living nearby in an apartment?

My take is that while these ridehail drivers are contributing an outsized share of charging sessions and revenue to charging networks, their increasing usage could become an issue, potentially causing friction between ridehail and non-ridehail drivers.

2) A positive trend for both EV drivers and charging networks/CPOs is EVgo’s reported higher charge rates of 47 kW in Q2 2024 from 42 kWh in Q2 2023. While EVgo did not explain this increase, it appears to be a combination of EVs becoming capable of charging at higher kW power levels, which equals shorter sessions. And an increase in the number of higher-power 350 kW charging dispensers.

3) A negative trend EVgo cited, however, is that of larger, less-efficient EVs. Presumably, these are EVs such as the GMC Hummer EV, Chevrolet Silverado EV, and the Ford F-150 Lightning. These trucks have very large batteries and weigh a lot resulting in lower efficiency which leads to longer charging sessions. As these less-efficient EVs grow in popularity, they are positive for charging networks and CPOs with higher kWh charging sessions and additional revenue, but this also means fewer available charging sessions and potentially longer wait times for other EV drivers.